A Spot Bitcoin ETF!

Exploring Interest, Potential AUM, and Price Impact

The price trajectory of Bitcoin is currently dominated by the prospects, or rather, the perceived odds, of the launch of a US Spot Bitcoin ETF. Judging by recent price increases and the results of two social media polls, approval should be considered a (potential) game-changer for Bitcoin. This post is aimed to rise above the noise and provide some useful insight into what a spot Bitcoin ETF may mean.

Why Spot?

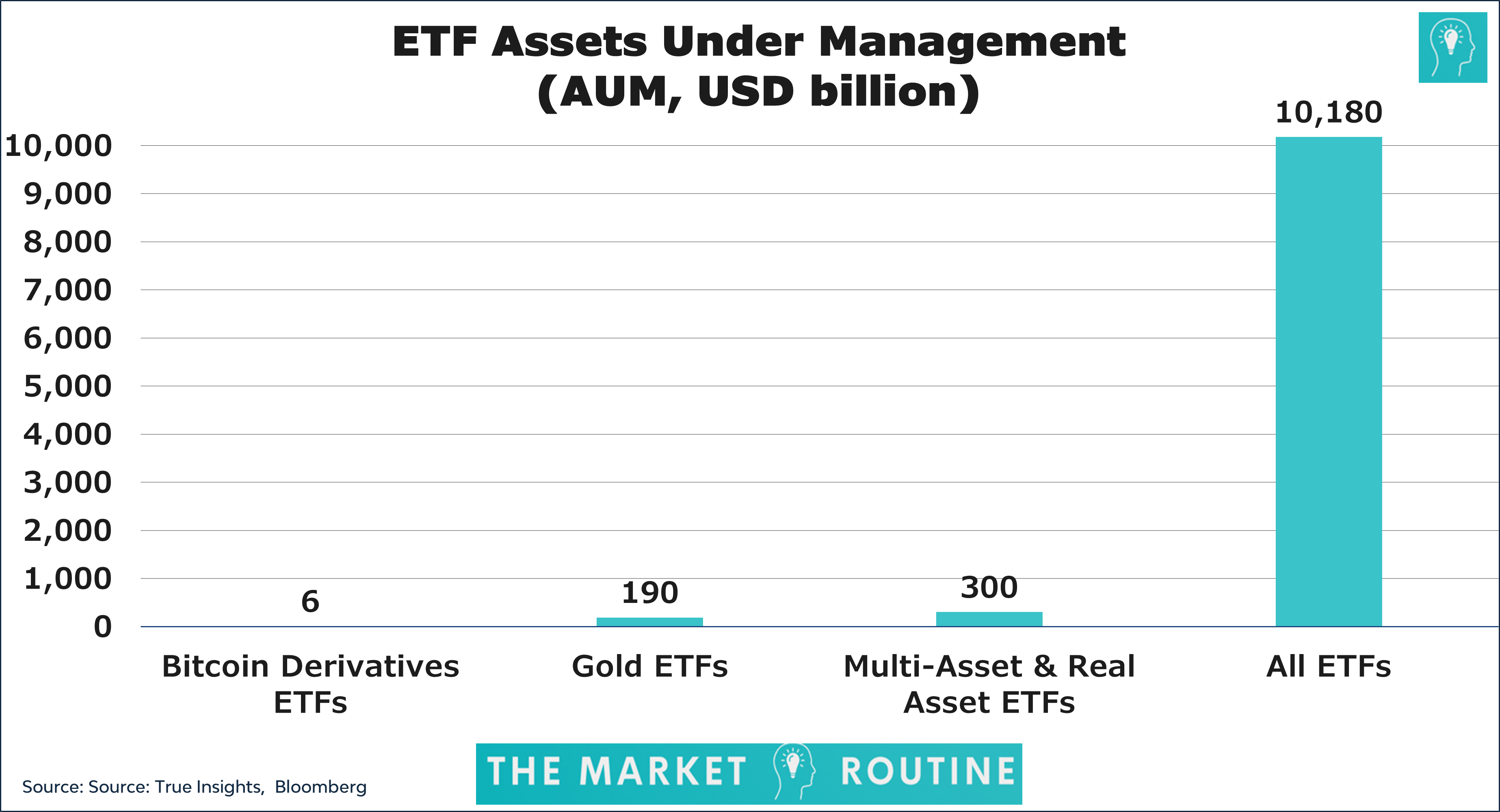

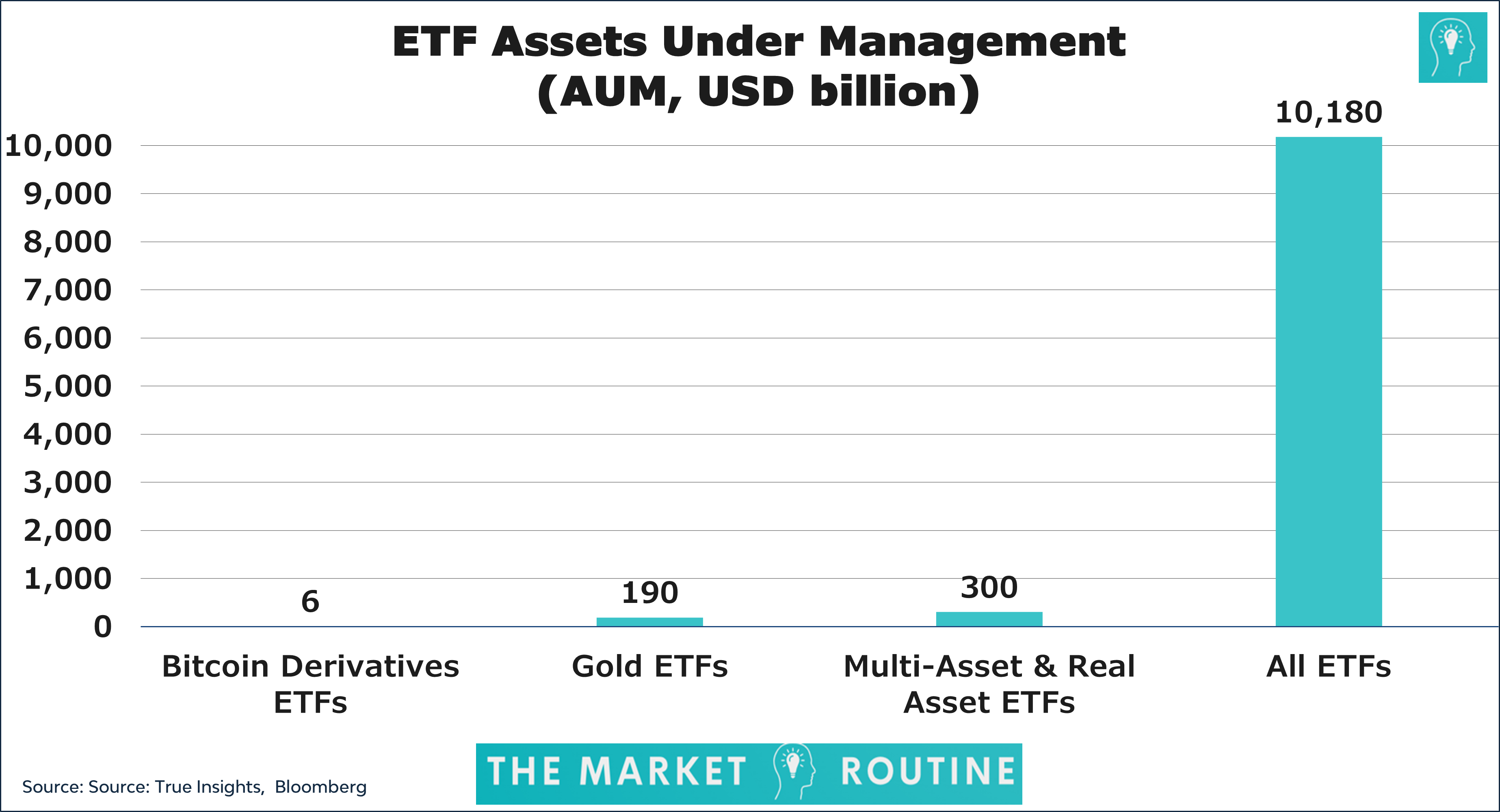

Before delving into the numbers, let’s briefly discuss the ‘need’ or ‘desire’ for a spot Bitcoin ETF. Such an ETF would invest directly in the 19.5 million Bitcoins currently in circulation, as opposed to Bitcoin derivatives like futures. ETFs based on Bitcoin derivatives or those tracking Bitcoin’s performance indirectly are already (widely) available, with combined assets under management (AUM) of just under USD 6 billion. However, for a significant group of investors, derivative-based Bitcoin ETFs do not meet their investment criteria.

Bitcoin, like physical gold, exists outside the traditional financial system. It is no secret that many Bitcoin enthusiasts, sometimes to an extreme extent, are concerned about the amount of money in circulation, the growing role of central banks, and the ever-increasing debt pile. While I don’t anticipate an immediate collapse of the current system – especially with central banks having ample room to cut interest rates again significantly during the next recession or crisis – it would be naive to ignore the risks associated with current fiscal and monetary policies.

From a risk diversification perspective, a spot Bitcoin ETF investing in Bitcoin outside the current system is more appealing than a derivatives Bitcoin ETF. However, investors should take into account that the legal structure of a spot Bitcoin ETF, including the issuer (e.g. BlackRock) and the custodian (e.g. Fidelity), is, in most cases, partially or entirely within the traditional financial system. This means that for a group of investors, a spot Bitcoin ETF will not be sufficient, for reasons I can relate to.

For the sake of completeness, I focus on ETFs here and not on other related investment vehicles such as ETCs (Exchange-Traded Commodities) or ETPs (Exchange-Traded Products), which sometimes use the term ‘physical’ in their name but often do not directly invest in Bitcoin.

Bitcoin Polls

Not every investor eagerly awaits the approval of a US spot Bitcoin ETF, as evidenced by two recent polls I conducted: one on X (formerly Twitter) and one on LinkedIn.

In the X poll, nearly 36% of respondents preferred other ways to invest in Bitcoin. Theoretically, these investors might prefer to invest in Bitcoin derivative ETFs. Still, it is much more likely that they would rather invest their Bitcoin outside the current system (e.g. in a physical cold wallet).

In the LinkedIn poll, a quarter of respondents preferred an alternative method of investing in Bitcoin. This difference is primarily explained by the fact that 40% of those surveyed in the LinkedIn poll expressed no interest in Bitcoin. This is not surprising, as my X follower base consists mainly of retail investors and Bitcoin enthusiasts, while my LinkedIn followers are predominantly investors in traditional markets. Bitcoin has not yet penetrated that investor base.

Maiden Investors?

However, what matters here are the shares of respondents answering ‘Yes.’ In both polls, nearly a third of respondents indicated they would invest in Bitcoin once a US Spot Bitcoin ETF has become available. This is more than I had expected and underscores the opportunity that a spot Bitcoin ETF presents.

Are these all new investors? Probably not. As explained above, Bitcoin investors currently in a Bitcoin futures ETF will likely switch to a spot variant. Why invest in a derivative if you can ‘own’ the real thing? However, the poll results and the current market cap of Bitcoin futures ETFs suggest that the approval of a spot Bitcoin ETF will attract new investors. The mentioned USD 6 billion in derivative Bitcoin ETFs represents less than 1% of Bitcoin’s total market capitalization (USD 660 billion at the time of writing). More data on the shares of ETFs in regular asset classes will reveal that 1% is extremely small.

Putting a Number on It

Estimating how much AUM spot Bitcoin ETFs can generate is far from straightforward, so any figure, including mine, should be taken with a grain of salt. This is even more applicable to price predictions derived from these estimates.

Let me start by saying that generating an estimate based on the total global (institutional) invested assets, as I have seen multiple times, including from a well-known three-letter investment house, or based on a list of AUMs of the largest ETF providers, seems somewhat simplistic and optimistic. As my polls demonstrated, many investors have no interest in Bitcoin, which should be factored in.

I will explore two alternative paths to arrive at a more ‘sophisticated’ AUM estimate.

Approach 1: Multi-Asset & Real Asset ETFs

I expect that investors in multi-asset ETFs and ETFs investing in real assets such as commodities and gold will be among the first to consider a spot Bitcoin ETF. Not in the least because I’m a multi-asset investor, and I allocate toward Bitcoin.

According to Bloomberg data, the ETFs falling into these categories have a total AUM of approximately USD 300 billion. To put this in perspective, those USD 300 billion represents about 3% of the total AUM of all ETFs, which amounts to USD 10,180 billion. In other words, multi-asset and real asset ETFs constitute only a small part of the entire ETF universe. Bitcoin derivatives ETFs, with their modest USD 6 billion AUM, make up just 0.1%(!) of the total.

Based on my calculations regarding the correlation and volatility of Bitcoin within a multi-asset portfolio, I would expect that spot Bitcoin ETFs would initially represent somewhere between 2.0% and 5.0% of the total AUM of these multi-asset and real asset investors. This would result in a spot Bitcoin ETF AUM ranging from USD 6.0 to 15.0 billion.

The Big Picture

Obviously, the numbers above overlook a crucial point, one that especially applies to deriving potential spot Bitcoin ETF AUMs based on a list of AUMs of the largest ETF providers.

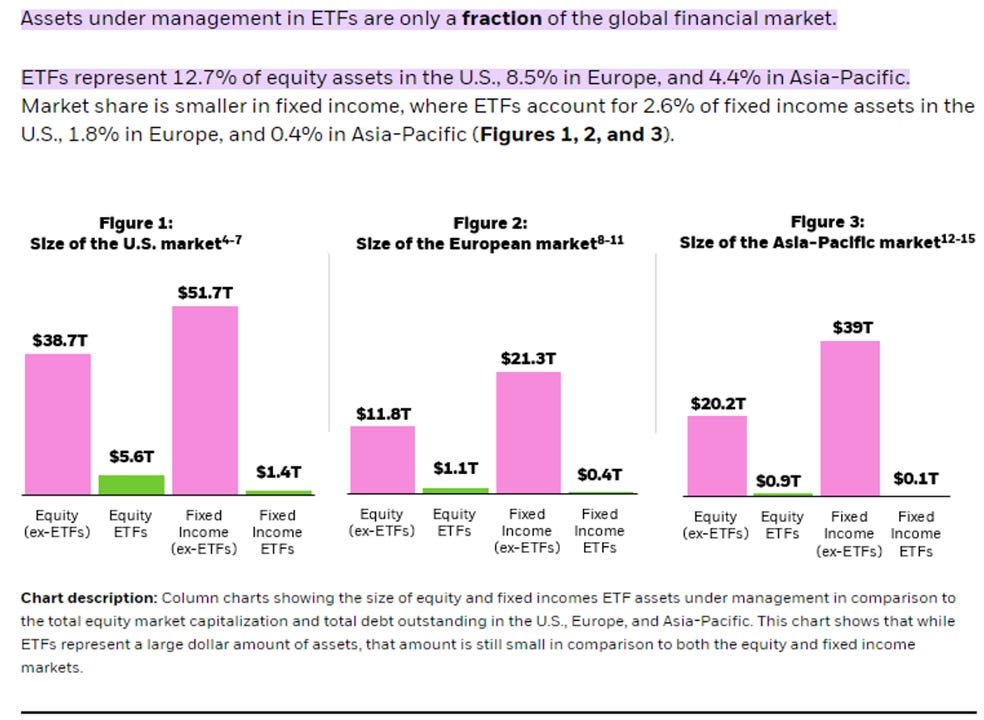

Despite media reports suggesting otherwise, ETFs still represent only a ‘fraction’ of the total global AUM. The chart below is from a post published on the iShares.com website on October 10, 2023, titled ‘Global ETF Market Facts: Three Things to Know from Q3 2023’. Hence, the data is very recent. The chart shows that in the US, ETFs account for 12.7% of all equity assets, while in the Asia Pacific region, it’s only 4.4%. Within fixed income, ETFs are an even smaller player, with a 2.6% share in the US and a mere 0.4% in Asia Pacific.

Total Investments

Unfortunately, no figures are available on the share of multi-asset and real asset ETFs of the total AUM invested in multi-asset and real asset investment solutions. However, using the iShares data from the chart and considering the weights of the US, Europe, and Asia Pacific in the MSCI World Index and the Global Bond Index, I estimate an ‘average’ percentage of the share of ETFs of the total AUM invested worldwide. That percentage is approximately 7%. In other words, I estimate that the total AUM invested in multi-asset and real asset solutions is 14 times larger than the total investments in multi-asset and real asset ETFs.

Making Sense of It

To get a better sense of this, I also looked at the AUM of gold ETFs compared to the total value of ‘investable gold.’ The latter is important because the focus here is on gold used as an investment (rather than, for example, as jewelry).

Based on recent data from the World Gold Council, and assuming that the majority of gold bars and coins should be considered investments and excluding gold held by central banks, the market cap of investable gold lies somewhere between USD 3,000 and USD 4,000 billion. If I take the midpoint of these two figures, gold ETFs (with an AUM of USD 190 billion) represent 5.4% of the total market cap of investable gold. This is pretty close to my estimate of 7% for ETFs’ share of all investments worldwide.

The First Estimate

If I work with that 7%, or a factor of 14, it suggests a total of USD 4,200 billion (USD 300 billion multiplied by 14) invested in multi-asset and real asset solutions. Again, assuming a Bitcoin allocation between 2.0% and 5.0% would result in a potential spot Bitcoin ETF AUM ranging from USD 84 to 210 billion. However, at this point, it would be wise to take into account the poll result indicating that a significant portion of respondents has no interest in Bitcoin. If I assume this group of investors to represent 33% of all investors, the numbers above should be multiplied by two-thirds (0.67), leaving a potential AUM ranging from USD 56 to 140 billion.

These AUM estimates can also be used to derive a Bitcoin price. Assuming that spot Bitcoin ETFs will also represent 7% of the total Bitcoin market cap – just as the weighted average for stocks and bonds – then the price of Bitcoin should be somewhere between USD 41,000 and USD 103,000. I reiterate that these are rough estimates strongly influenced by the assumptions made, but they do provide some guidance.

Approach 2: Going for Gold

Those who follow me will know that I see Bitcoin’s potential in digital gold first. An insurance premium (outside the traditional financial system) with a value attached to it – after all, insurance is never free. Physical gold, too, represents such an insurance premium. And in the case of gold, you can quantify it by looking at the gold-to-silver ratio. Gold is roughly 15 times scarcer than silver, yet its price is 85 times higher. The difference serves as an estimate of the insurance premium. Based on the numbers above, the insurance premium for gold stands just below USD 11,000 billion. Hence, most of gold’s market cap is reflected through its function as an insurance premium.

Time for another critical assumption. I expect that, in the long run, Bitcoin will represent 10%-20% of the total insurance premium of gold. Currently, that percentage is at 4%. While it is considerably lower than what the three-letter investment house mentioned earlier suggests, it is still significant.

However, it’s pretty straightforward to make either a case that Bitcoin will ultimately represent 0% of the premium (the asset fails) or that it will skyrocket to 100% (nobody wants to carry their heavy, easily stealable insurance premium around, all the gold in vaults gets confiscated, or Mars turns out to be loaded with gold).

With a 10%-20% share, we are talking about a Bitcoin market cap ranging from USD 1,100 to USD 2,200 billion. With an assumed 7% share of spot Bitcoin ETFs, this would result in AUMs ranging from USD 77 to 154 billion. You would arrive at Bitcoin prices between USD 56,000 and USD 113,000. These figures are not far from the first analysis.

Important Considerations

Aside from reiterating that these are rough estimates relying heavily on assumptions, there are two additional points I want to emphasize. First, the above analyses do not explicitly account for the group of investors who do invest in Bitcoin but do not want to do so through a spot Bitcoin ETF. I explained the main reason for this (truly outside the traditional financial system) at the beginning of this piece. If this is factored in, the potential ETF AUMs will be lower.

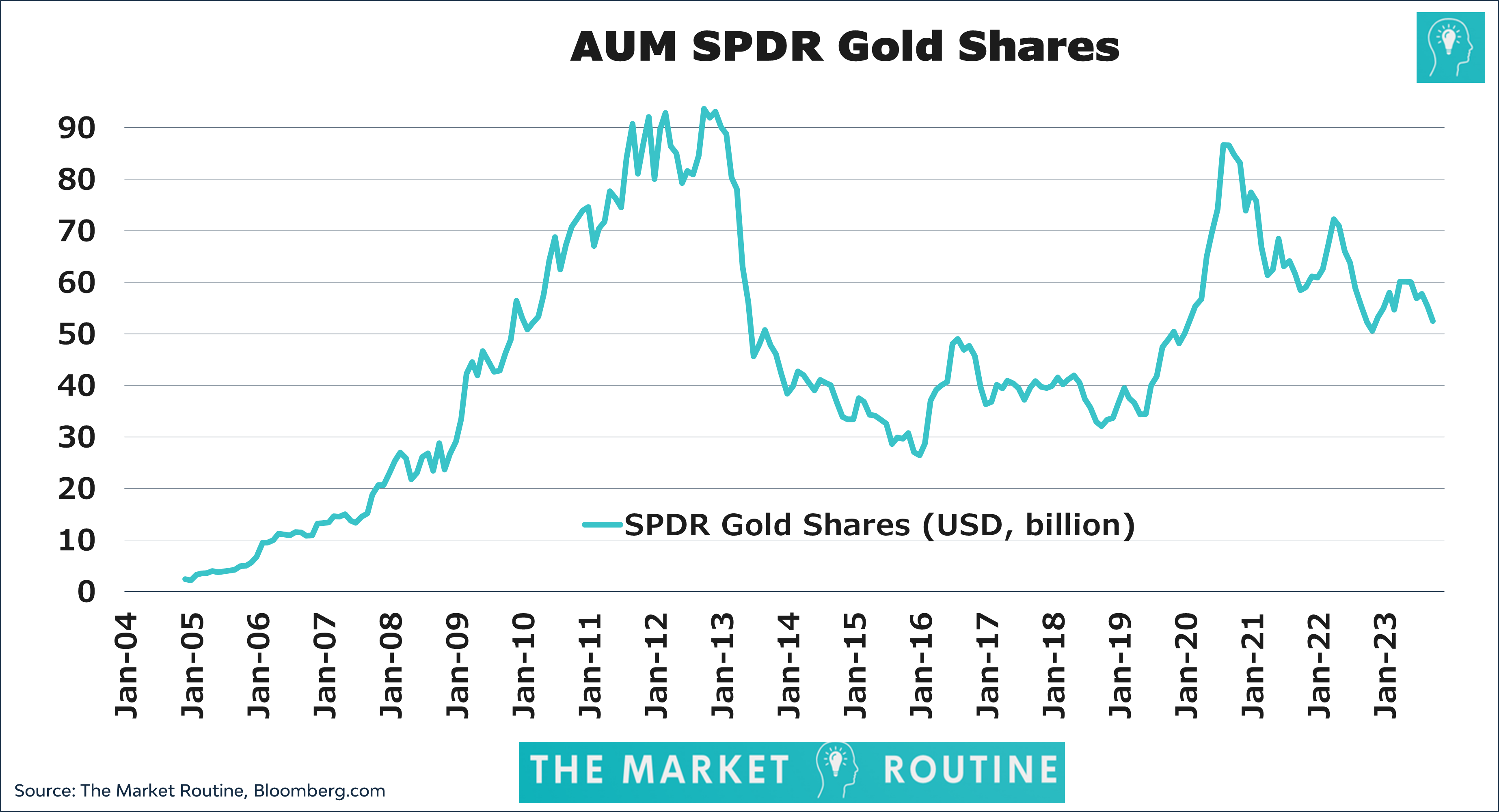

The second is ‘time.’ Estimates of potential spot Bitcoin ETF AUMs are ‘fun,’ but equally important is how long it will take for these AUMs to be achieved. To shed some light on this, I looked at the mother of all gold ETFs, SPDR Gold Shares. On November 18, 2004, State Street Corporation launched SPDR Gold Shares, the first-ever (US) gold-backed ETF, which surpassed USD 1 billion in assets within its first three trading days.

The chart below shows the AUM progression of SPDR Gold Shares. And ‘yes,’ I have adjusted the numbers for inflation. SPDR took barely four months to achieve an AUM of USD 10 billion (calculated in today’s dollars.) Within 14 months, it had reached the USD 50 billion mark. It did so including the launch of competitors like the iShares Gold Trust, founded in 2005. Currently, this is the second-largest physical gold ETF after SPDR, with an AUM of over USD 25 billion.

Please note that gold (even twenty years ago) is a considerably larger asset class than Bitcoin is today. On the other hand, there will likely be a slew of spot Bitcoin ETFs approved all at once. Nonetheless, I believe it will take considerably longer than 14 months for spot Bitcoin ETFs to break the USD 50 billion barrier. This also has implications for expected returns.

Volatility - A Positive Feedback Loop?

Finally, one could argue that, in a vacuum, inflows should not have a structural impact on an asset’s value. A structurally higher Bitcoin price may happen in many ways, but when the case has to be built on future AUM, there must be a link with liquidity and volatility. An endless series of empirical studies, especially focused on stock markets, demonstrates that less liquid assets have higher volatility, which is reflected in prices. In other words, the required risk premium is higher when an asset is more volatile. So, you want to see some form of a positive feedback loop between growing AUM, rising liquidity, and lower volatility.

And that Bitcoin’s volatility will decrease, something assumed by many Bitcoin pundits, is not a given. A simple analysis shows that after the launch of SPDR Gold Shares, the realized volatility of gold did not decline.

The significant growth of gold ETF AUM over time cannot be used as clear evidence for the (strong) increase in the price of gold since 2004. It is more likely that gold’s growing role as investment insurance has been accompanied by a higher value of the insurance premium. This narrative would be supported by the increase in the gold-to-silver ratio from 40 to over 80.

The same applies to Bitcoin. There must be a driving force, other than AUM, that pushes the price higher.

Final Words

Every estimate related to the potential AUM of spot Bitcoin ETFs and the resulting impact on the Bitcoin price should be taken with a substantial margin of uncertainty. I have tried here to provide some insight using existing statistics, such as the share of ETFs in total global investments and the insurance premium value attached to gold. Based on the outcomes of my Bitcoin polls, where a significant one-third of respondents expressed interest in investing in a spot Bitcoin ETF, the approval of such an investment solution will likely be a game-changer. This is something I have underestimated, considering Bitcoin’s appeal as an asset that operates outside the traditional financial system.

Nonetheless, I hope this analysis offers a somewhat nuanced perspective on the possible developments concerning an asset class that still evokes extreme opinions and views. However, with the introduction of a traditional investment solution, these extreme opinions are likely to become more tempered.

These are always adeptly created and insightful pieces