No More Triple-A for the US - The Major Consequences of Debt Sustainability (Part II)

The available solutions to preserve debt sustainability will result in a shift toward real and scarce asset classes.

I am somewhat surprised by the fierce reactions from ‘traditional’ economists and investors dismissing Fitch’s decision to strip the US of its AAA rating as nonsensical. A frequently used argument is that no market on the planet can rival the US Treasury market. Not in terms of size, liquidity, or its role as a haven in times of turmoil. If there are doubts about the US meeting its debt obligations, there should be doubts about every other country. The prevailing thought of the downgrade opponents is that if the US no longer deserves an AAA rating, then no one does.

Unique does not equal Limitless

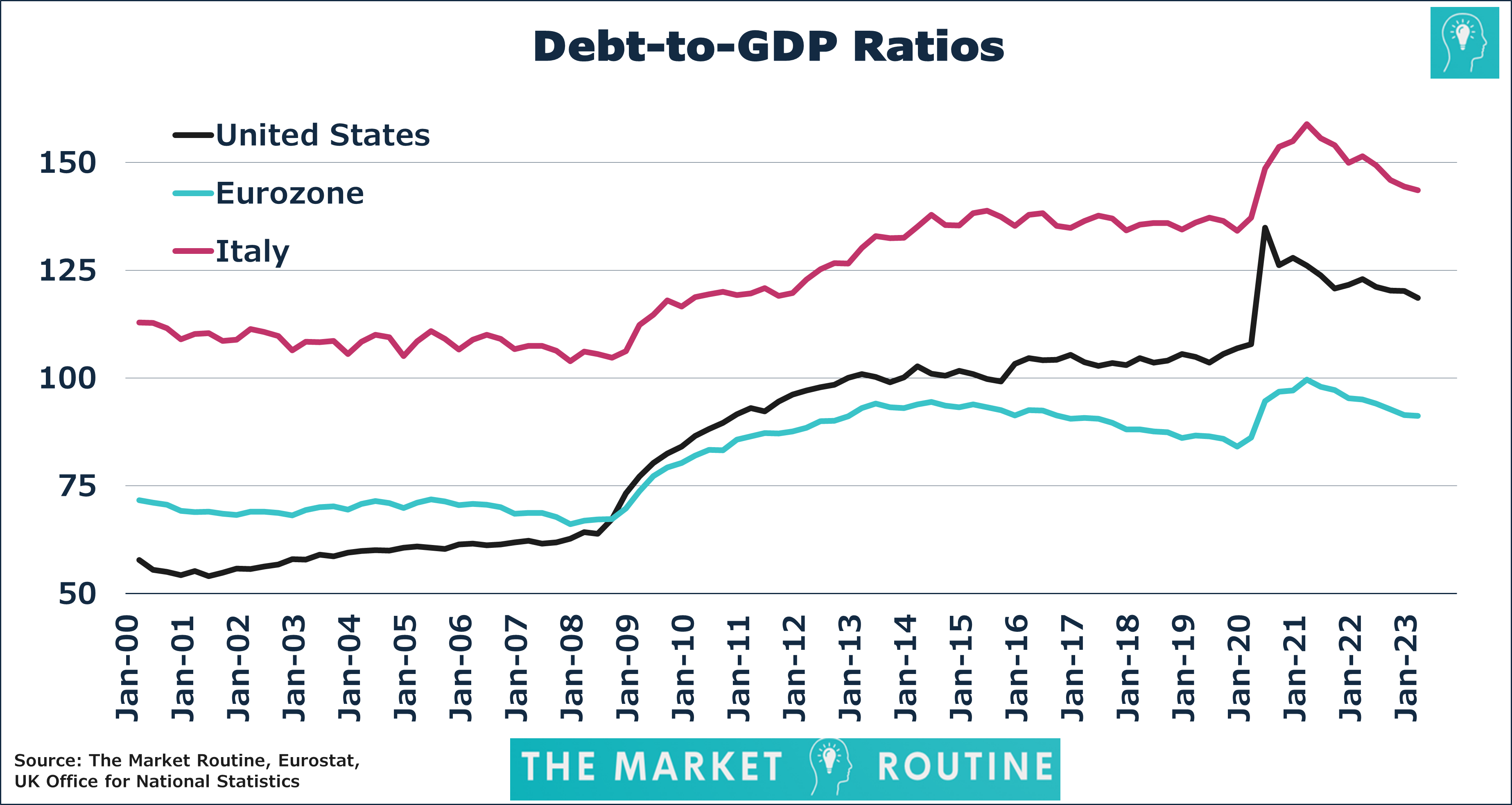

While I do agree with the unique position of the US Treasury market, it goes too far to conclude that there is essentially no limit to the US budget deficit or the debt-to-GDP ratio. In recent years, it has become evidently clear that a rapidly growing group of investors is increasingly concerned about the ever-rising mountain of global debt and the sustainability of the current financial system.

Moreover, over the past decades, examples have surged that the rising trend in debt-to-GDP ratio is not unique to the US. Around the globe, we can observe spiking debt levels after every (financial) crisis, never returning to pre-crisis levels. Apart from the upward trend in debt-to-GDP ratios, the Italian bond market is in no way comparable to that of the US. Hence, Italy now requires external assistance to facilitate its spiking debt levels, resulting in the ECB de facto buying every Italian bond during each new crisis. Yet the central bank stubbornly denies that debt sustainability is a primary policy target. The debt sustainability issues of Eurozone countries lacking a safe haven bond market status also explains why economists and central bankers are considering the issuance of Eurobonds. This distributes the issue of debt sustainability across member states, including those with the lowest debt-to-GDP ratios and deepest bond markets.

How to maintain Debt Sustainability?

Yet, even for the US, ensuring debt sustainability is a pivotal question. I recently conducted a poll on X (formerly Twitter) and LinkedIn, asking what is the ‘best’ solution for reducing elevated debt-to-GDP ratios. Both polls yielded similar results.

Approximately a quarter of respondents think that the most important solution is faster economic growth, and roughly the same percentage chose austerity measures. But even though these answers are ‘obvious,’ the big question is how feasible they are. Potential GDP growth is decreasing in many parts of the world due to an aging population.

A structural increase in productivity growth could offset this declining trend, for example, through a fourth ‘industrial revolution’ powered by Artificial Intelligence. However, especially in the short term, it’s easy to overestimate the impact of AI on economic activity. In addition, it’s fair to conclude that the third industrial revolution – driven by the internet – failed to reverse the declining trend in economic growth.

Unless you expect growth miracles from AI, austerity quickly comes to mind as the next ‘viable’ option to reduce debt. Unfortunately, austerity lacks both societal and political support. The necessary spending cuts would have to go far beyond a more efficient and smaller government. Structurally lowering debt-to-GDP ratios requires widespread austerity measures, including politically sensitive areas like social security, healthcare, education, pensions, and defense. While the importance of these categories varies by country, they share that politicians are unwilling to make spending cuts in these areas the focal point of their election campaigns. Achieving a lower debt-to-GDP ratio through structural spending cuts in these areas is highly unlikely.

Feasible Alternatives

Therefore, alternative, politically more realistic solutions will be looked for. And these include persistent low interest rates and structurally higher inflation.

Of these two, lower interest rates have been applied for many years already. Quantitative Easing has become central banks’ default ‘solution’ to counter crises, deflation, and defaults (e.g., Greece, Italy). The result of the ongoing expansion of central bank balance sheets is always the same: lower interest rates. Additionally, the ECB has demonstrated that central banks will not shy away from implementing negative interest rates. Structural low interest rates maintain debt sustainability, with few opposing as they benefit businesses and consumers. Low interest rates also explain why the global economy is not in recession even after the most significant tightening cycle since the early 1980s.

A structurally higher inflation level seems a more undesirable alternative after the price spikes we witnessed in recent years. Nevertheless, I think higher inflation will become part of maintaining debt sustainability. Theoretically, central banks can think of ample reasons to justify an increase in the inflation target. For example, persistent supply chain bottlenecks (partly due to deglobalization,) a rising likelihood of structurally higher energy and food prices (also partly due to deglobalization), and a structural shift in labor market supply and demand. In addition, central banks may refer to climate goals that lead to a structurally higher demand for raw materials. It’s no coincidence that the ECB already incorporates ESG criteria into its policies, even though its current mandate hardly allows this.

A Future-Proof Investment Portfolio

Most investment portfolios reflect almost four decades of declining inflation. During the last 40 years, many have predicted the end of the traditional 60-40 portfolio (60% stocks, 40% bonds), only to be proven wrong. A traditional investment portfolio composed of stocks and government bonds has performed exceedingly well in the past. Consequently, most portfolios consist mainly of these two asset classes.

However, when allowing for structurally lower interest rates and higher inflation in the long-term outlook, it’s questionable whether the traditional 60-40 portfolio will hold up. In the case of structurally low or even negative interest rates (think of real rates adjusted for inflation), nominal bonds lose a lot of their historic appeal. Gold, on the other hand, will thrive under these circumstances. The correlation between the gold price and real interest rates is extremely strong. Falling rates result in higher prices and vice versa. In addition, I expect investors to seek smarter ways to ‘hold’ cash. The opportunity costs of holding cash increase as inflation rises. Investors will look for low-risk alternatives to cash to escape the erosive effects of inflation.

More risky asset classes like stocks will also benefit since low rates force investors to increase risk to achieve their return goals. Bitcoin, which comes with the potential to mirror gold as an insurance premium against ‘unpleasant events,’ also fits into this category. Obviously, these unpleasant events vary for each investor, but that’s beyond the scope of this analysis.

With structurally higher inflation, commodities and gold come into play. Historically, these investment categories provide decent inflation hedges. Generally, scarce investment categories will become more attractive because they keep their value when inflation rises. Bitcoin also adds to the list of scarce asset classes, along with art, classic cars, wine, etc. However, unlike Bitcoin, investment opportunities for the latter categories are limited, even though they are increasing. Inflation-linked bonds will appear on the radar for investors with lower risk tolerance. And as long as inflation doesn’t become unanchored – which is a key risk when increasing the inflation target – equities and real estate will remain attractive asset classes. As the past years have shown, many companies can pass on higher costs to their customers. Investing in stocks mitigates the strain of higher inflation experienced as a customer.

Adaptation

Real and scarce investment categories are heavily underrepresented or absent in most investment portfolios. I expect this to change. Investment portfolios incorporating the few alternatives to maintain debt sustainability – low interest rates and higher inflation – will look different from their predecessors. Gold seems destined to play a bigger role in these future-proof portfolios. But there’s also a case for commodities, real estate, and Bitcoin. In addition, I expect equities to continue to play a significant role in future multi-asset portfolios. Hence, combining traditional with alternative asset classes is the way to go. The beauty is that these traditional and alternative asset classes will accomplish what every investor should have at the heart of their investment framework: diversification.