The End of an Empire?

The End of an Empire?

The U.S. will not default, but its massive debt does require you to move away from bonds

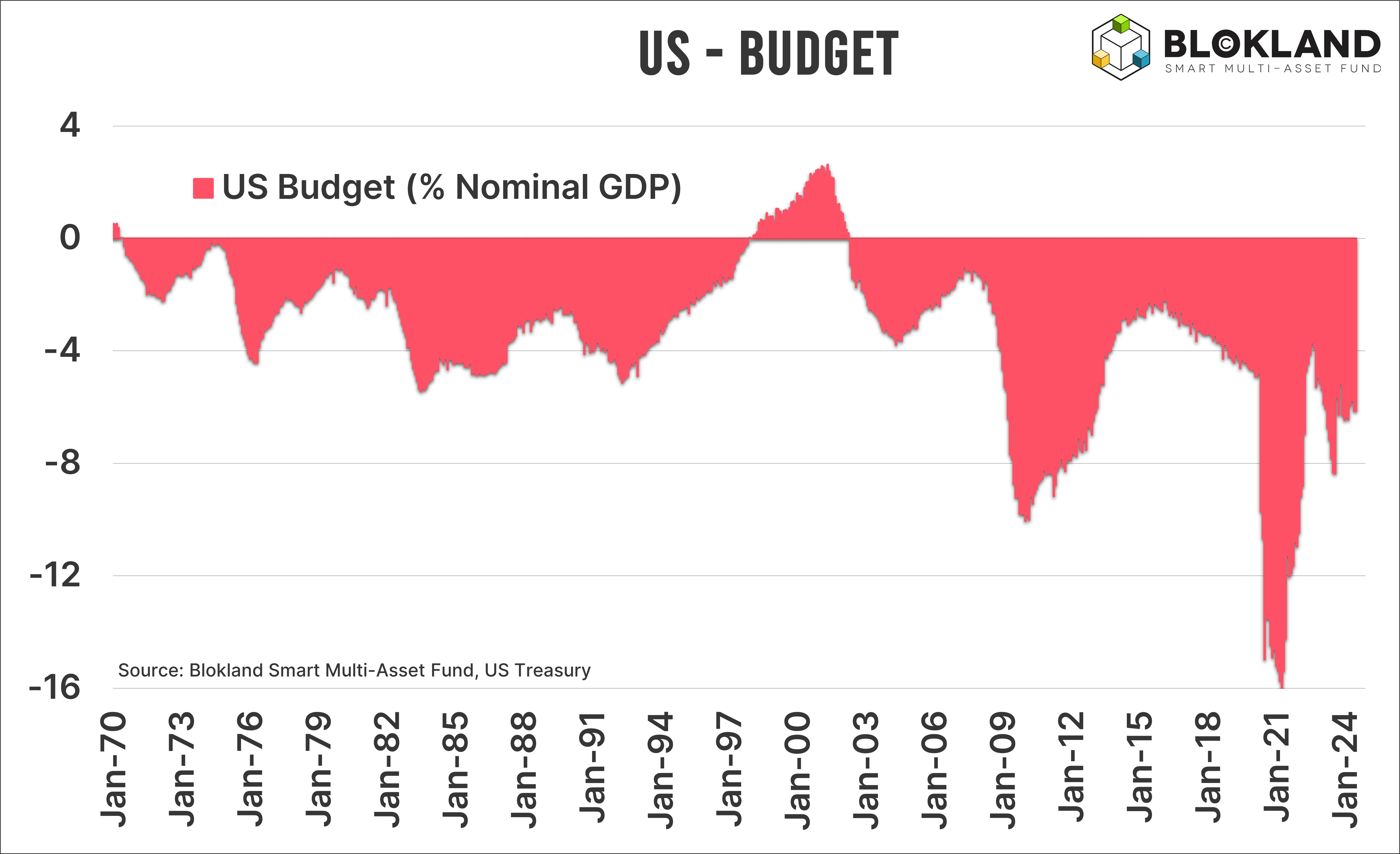

I recently came across a graphic on the Wall Street Journal's website titled "Will Debt Sink the American Empire?" And it's not an isolated case. As the United States heads toward yet another exorbitant budget deficit of 7% of GDP, grim debt charts are popping up everywhere. While a U.S. default is unlikely, the implications are significant for investors.

Pre-paid asset

For many investors and economists, budget deficits are not a concern. Their rationale is simple: when the government issues debt, thus creating a liability, that debt must appear as an asset on a balance sheet elsewhere. And that's literally where the story ends.

I struggle with this logic. It's not because assets and liabilities must balance to zero, but rather the assumption that this completes the narrative. In reality, the roller coaster just begins. Once you ask the pertinent question of whose balance sheet all this great debt will end up on, you will realize that 'willingness' plays a crucial role in the dynamics between debt, interest rates, and, ultimately, central bank policy.

The Trinity

For any investor, three factors make up the trinity of sound investing: return, risk, and diversification. First, it's clear that despite a series of rate hikes by central banks, current interest rates are far from elevated. Considering that inflation will likely be between 2% and 3%—rather than the 1% to 2% we've seen between the Great Financial Crisis and COVID — real returns do not look great. In addition, to quell concerns over massive deficits and debts, central banks' default option is to keep rates low, not high.

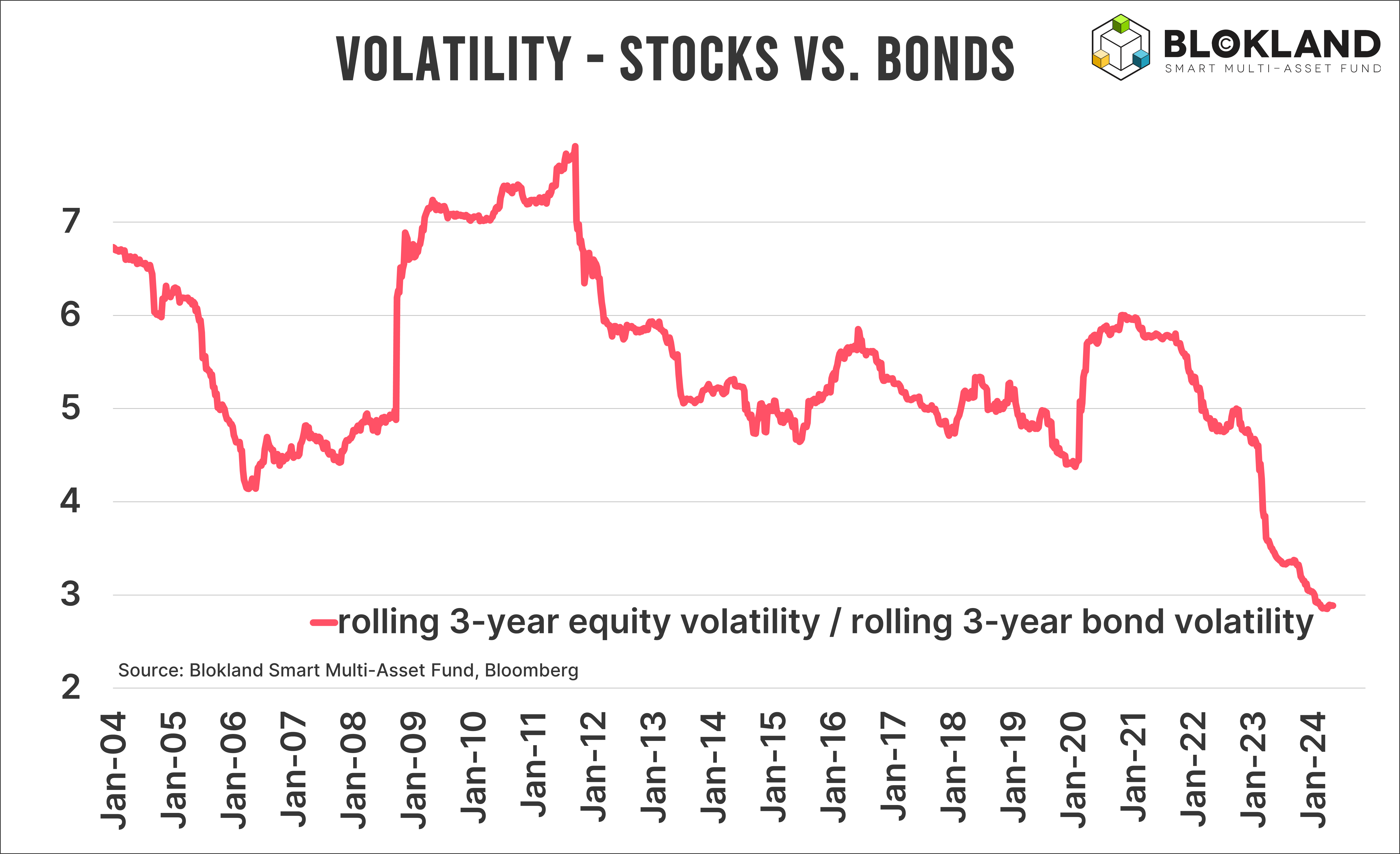

Second is risk. Realized volatility on (government) bonds is steadily increasing. This is true for the United States, but even more so for countries like France, Italy, and Japan. Collectively, these nations account for about 50% of global government debt. If you compare the volatility of bonds to that of other asset classes like stocks, any mean-variance optimization 'expert' will tell you immediately what will happen to the 'optimal' allocation towards bonds. Down!

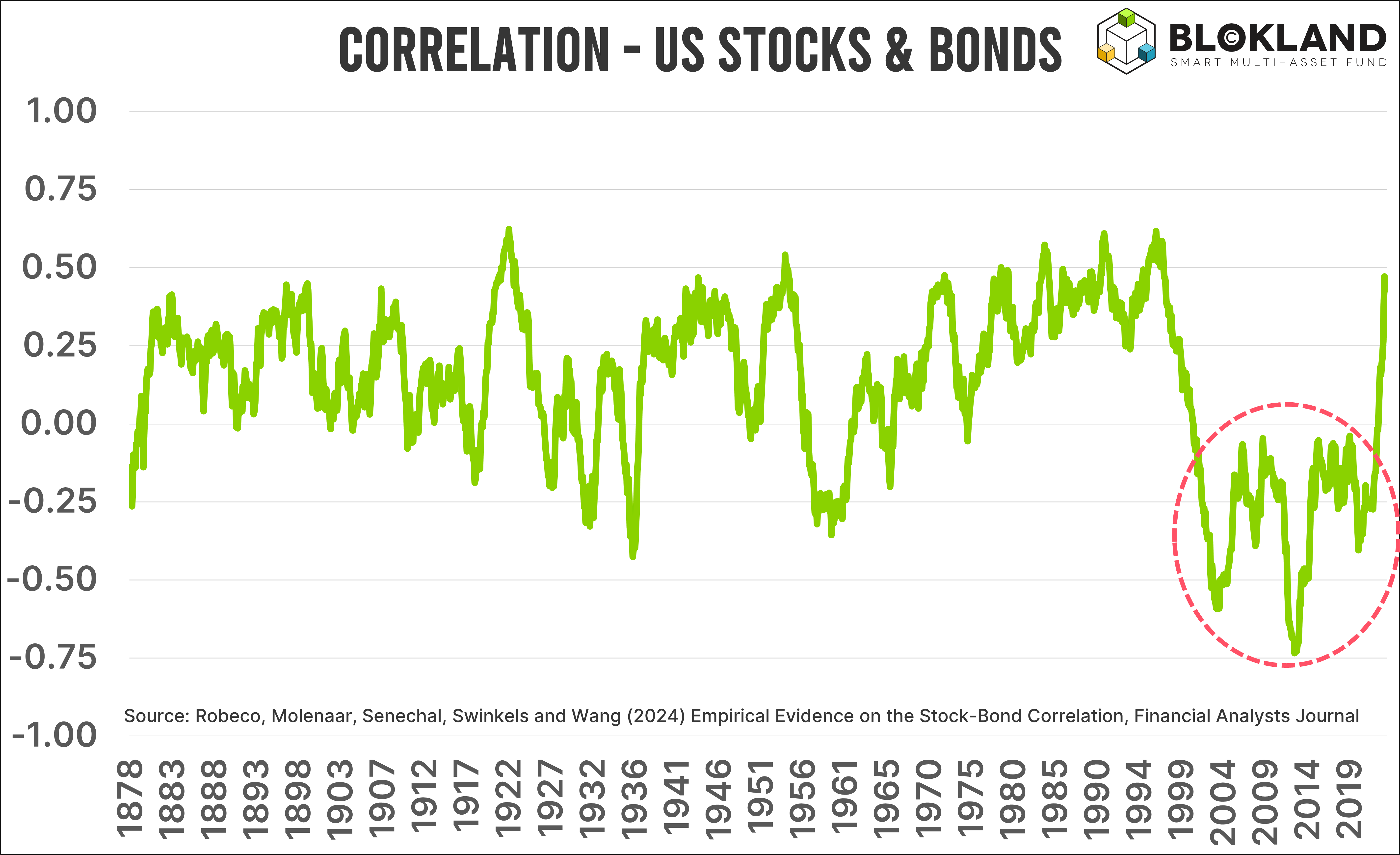

Finally, diversification. From 1990 to 2020, the correlation between stocks and bonds was negative. However, contrary to what many investors think they know, that was the exception. The correlation was consistently positive in the 110 years before, which means the diversification benefit of bonds has been grossly overstated.

Based on these three factors, any self-respecting investor should at least question the attractiveness of investing in bonds. This is aside from the willingness of countries like China, which have different motivations for reducing their investments in U.S. Treasuries.

Crystal Ball

You don't need a crystal ball to forecast what will happen. The U.S. is not going to solve its debt problem any time soon, if at all. And considering the 'old men' battling to lead the world's most powerful country, and their dreadful track record regarding budget deficits, don't be surprised if things get worse. Nonetheless, the U.S. won't go bankrupt, contrary to what the headline of the Wall Street Journal might suggest.

Instead, the central bank' kicking the can down the road' model will continue to prevail. On average, low interest rates combined with higher inflation will stretch (perceived) debt sustainability. To achieve this, the willingness of central banks to buy bonds will be tremendous, resulting in a negative impact on the trinity of sound investing. The situation is way more delicate for other countries, lacking a world reserve currency and the deepest, most liquid bond market that also provides collateral to banks globally. I will leave those countries for another time.