Vive La France!

Vive La France!

The outcome of the European elections confirm bonds are an inferior asset.

According to traditional media, investors are shocked by the outcome of the European elections. European financial markets took a nosedive, largely attributed to the sharp swing to the right. But that's just looking for a stick to beat a dog with. It's not the first time that, amidst increasing uncertainty, investors seize upon long-known weaknesses to offload their investments.

Notorious Offender

Based on developments in recent years and numerous election polls, it could hardly have been a surprise that 'right-wing' parties were going to make significant gains. Nevertheless, the victory of the Rassemblement National in France, with more than 31% of the vote, was so big that the current president, Macron, felt compelled to call for early elections. This is a common tactic used by politicians trailing in the polls to regain political momentum.

This move resulted in a sharp drop in the euro, French stocks lagging well behind the European and global average, and the spread on French 10-year bonds rising to its highest level in over seven years. The often-parroted argument is that due to this political shift, investors are now (suddenly?) concerned about fiscal discipline in France.

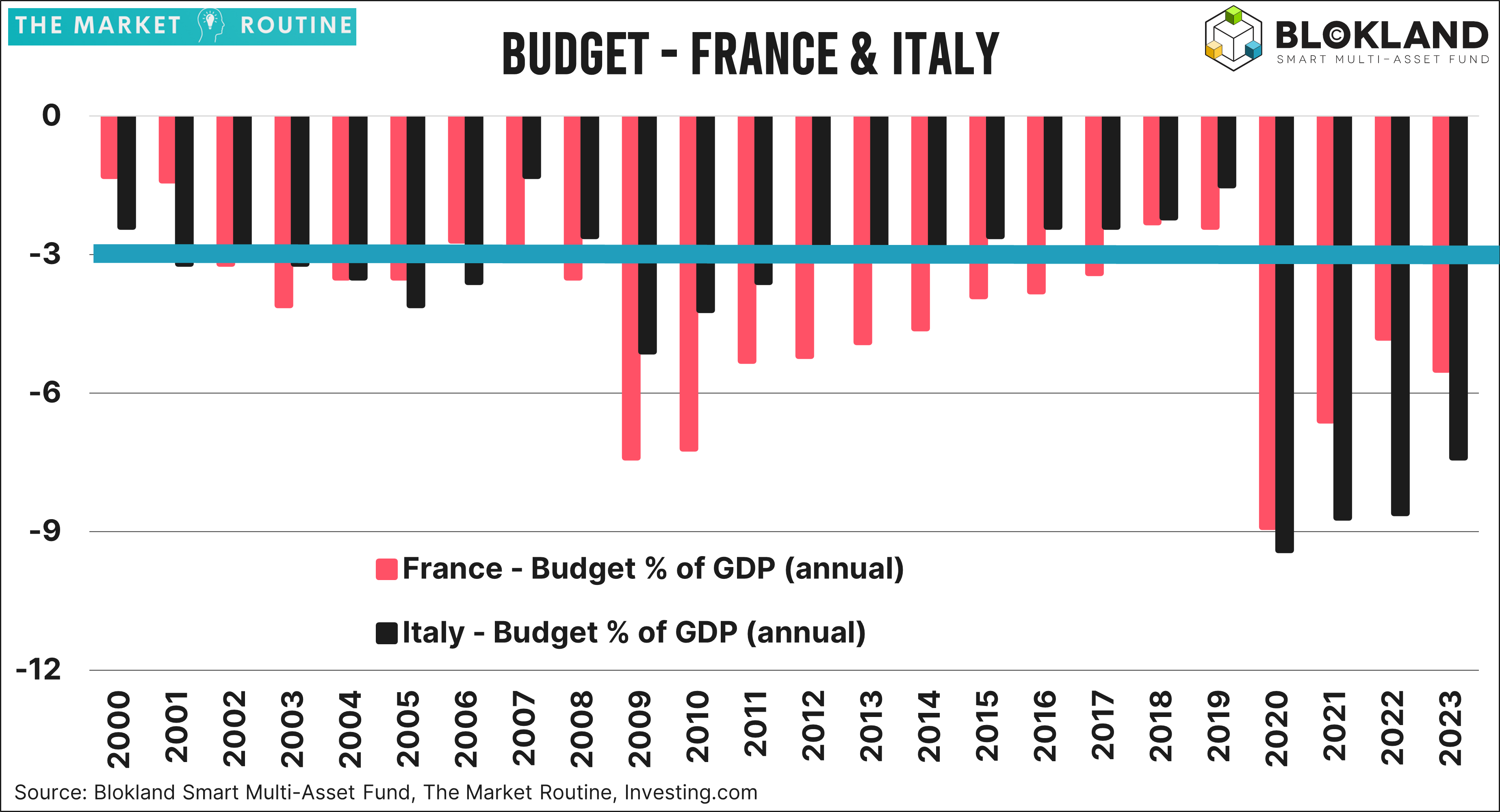

However, fiscal sustainability has always been a concern. Regardless of who is in power, France consistently mismanages its budgetary policy. The chart below shows France and Italy's annual realized budget deficit – a surplus simply never occurs.

As is blatantly clear, France is a notorious repeat offender regarding budget deficits. In the sixteen years since the 'Great Financial Crisis,' France has managed to keep its deficit below the once 'holy grail' of 3% of GDP only twice. The average annual budget deficit over that period is 5% of GDP. By comparison, Italy kept the deficit within the 3% limit in eight of those sixteen years. To be fair, it took an existential threat and near-collapse of the Eurozone – which was, incidentally, quelled by an Italian speaking the words 'whatever it takes' – but still.

Uncertainty

In my view, we need to see the market reaction in a broader context. The election results create uncertainty. And markets hate uncertainty because it knocks them off their pink cloud and forces them to deal with risk. If those same markets have seen my deficit chart, they cannot be happy, especially since France will again not have its budget in order this year. And what do you think Macron will do to win back those voters? He'll dangle a carrot in front of them, which must be paid for.

You can debate it at length, but a polarizing political climate, with more significant shifts from left to right and vice versa, is a recipe for budget deficits. Not to mention that inherently large expenses like social security, pensions, education, healthcare, security, and so on, keep increasing.

Fortunately, the ECB has already lowered interest rates. I suspect that Christine has my chart hanging on her fridge, too.